Investing seemingly as a Game of Coin Toss

A recent Twitter post by Michael Maubossin of Morgan Stanley to demonstrate the role of randomness via a coin toss exercise with his students in his university class, sparked this article and got me to think deeper and think about it, from a statistical point of view.

“Like other finance professors, I did the obligatory coin toss exercise with my students @Columbia_Biz last night to demonstrate the role of randomness. One student called 9 correctly in a row. Yeah, don’t bother: her fund is now closed to new investors.”

Let’s delve deeper…

We don’t have the specifics of Maubossin’s assumption in the coin toss exercise in his university class, but let’s assume the following, which are likely to be fair assumptions.

- Probability: 50% equal probability of heads or tails (i.e. the coin is fair and not loaded/biased and that represents equal probabilities of either winning or losing)

- Payoffs: Same magnitude of gain or loss. Heads provides a fixed positive payoff and Tails provides a corresponding negative payoff of the same magnitude.

- Independent: Each coin toss (i.e. outcomes of either Heads or Tails) are 100% independent of each other. Previously historical tosses have absolutely zero influence on result or predictability of any future coin tosses / outcomes.

- Sample Size: The sample size is large enough. The class would probably be between 20–50. But let’s assume the sample size is large enough to approach the law of large numbers, and that observations & corresponding conclusions can thus be valid to infer.

Randomness & Top Performers

With a sufficiently large number of participants (i.e. sample size) and a large number of rounds of coin tosses, eventually the results of the coin toss exercise are likely to head towards a normal distribution that looks like one below.

Thus one should not be surprised to see that in this exercise, there is a high likelihood that there would be one student (at least one, or even none) who can get keep getting all the calls right consecutively. And in this case, that specific student calling it right 9 times in a row. The initial conclusion is that top performance is only, but a consequence of randomness (or luck), and that this exercise if done repeatedly often enough, would likely yield similar observations.

A classical thinking is that in all randomness and in the right tails, there will always be stars and top performers.

Investing is no coin toss exercise

However, there is far more in investing that extends beyond the simple coin toss exercise. The coin toss exercise seemingly oversimplifies investing performance somewhat. Let’s attempt to explain why it could be so.

Investing is a game of games, and there are many games within games.

This applies specifically to investing in stocks for the long-term, i.e. a buy and hold strategy with little portfolio turnover, no short-term trading, leverage, short-selling, and the utilisation of any derivatives, be it options, which is also what we do at Vision Capital.

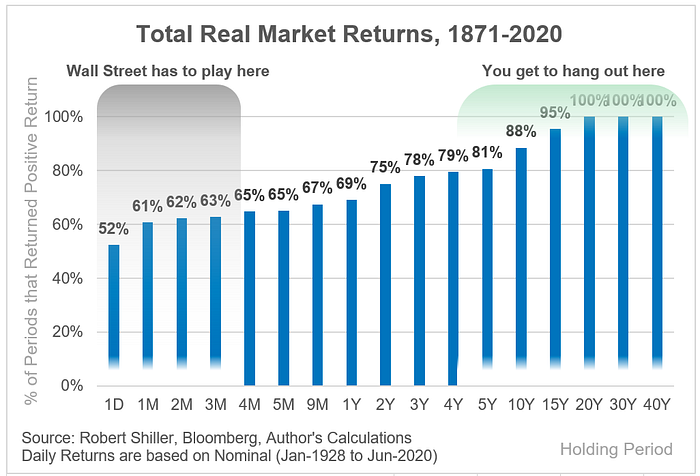

(1) Probability of Winning and Losing is not 50%

Probability: The probability of winning or losing in long-term investing is not 50%. From the chart below, the probability is close to 50%, more specifically ~52% on average if you buy and hold a stock for 1 day. However, if your investment holding period is 5 years, the probability of a stock investment returning a positive return is ~81%, and this rises to ~100%, if the investment holding period is extended to 20 years and beyond.

(2) Payoffs are Asymmetric, not Symmetric

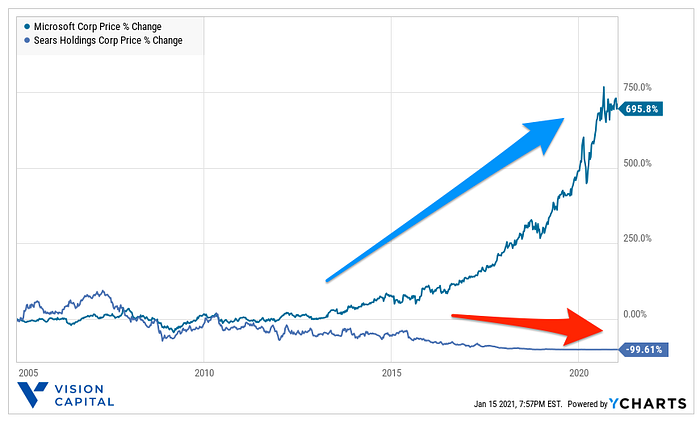

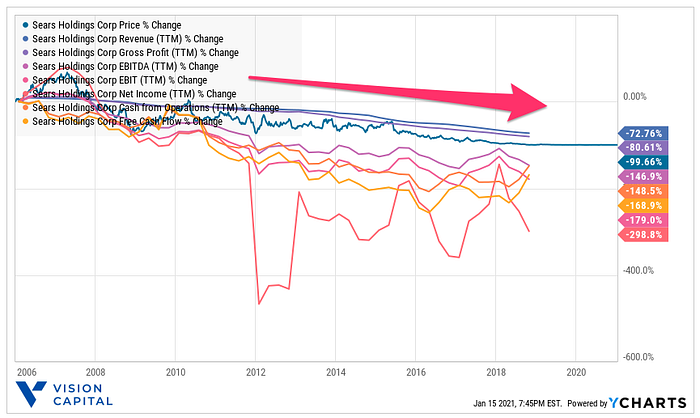

The maximum downside a stock can lose is -100%. On the flip side, the maximum theoretically upside a stock can gain is unlimited, and in many winning stocks, they can end up being multi-baggers, 5X , 10X, 20X, 50X, 100X and beyond. This is differs drastically from the coin toss exercise, where the payoffs are symmetric and of equal magnitude.

Microsoft (7X @ +695%) vs Sears (-100%) is a case in point.

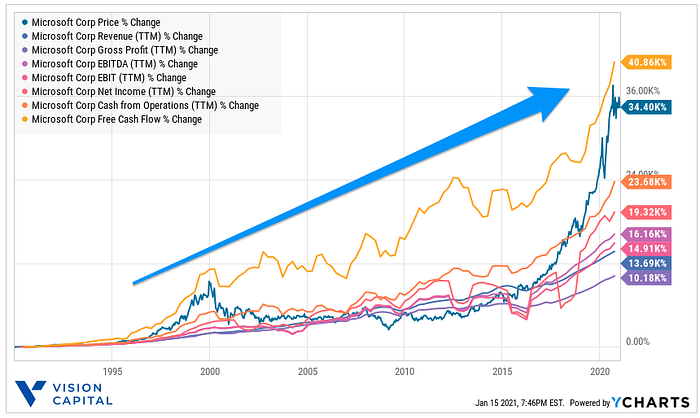

(3) Winners win and keep winning

If you are day trading stocks, your day-to-day outcomes are far likely to be more independent and random (although this can be skewed positively, if you are a great day trader.

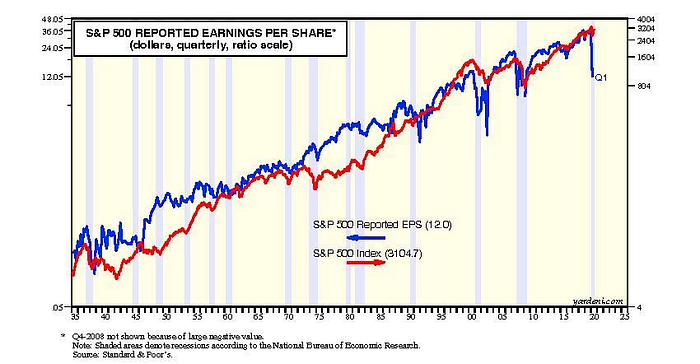

But if you are investing for the long-term, persistency does tend to occur, because the stock market is truly a voting machine in the short-run, but a weighing machine in the long-run. It is revenues, profits and cash flows that drive higher stock prices and vice versa lower.

It is because companies build great products and services and the positively reinforcing flywheel of growth can take them off to great multi-year success. Similarly, if the company is not winning customers, the deceleration of its business can similarly take a rapid downward spiral. The two examples of Microsoft and Sears illustrate the case in point.

Investing thus vastly differs from the independent coin toss exercise.

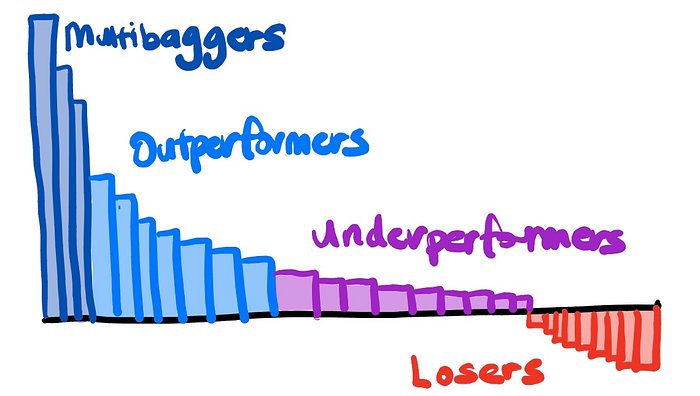

Winners tend to win, and keep winning. Let your winners run high.

Losers tend to lose, and keep losing. Let them go, do not chase after them.

In investing, if we keep focusing on playing in unfair fights where we position ourselves (1) to have a higher probability to win, with (2) asymmetric payoffs that are in our favour such that when we win, we win big.

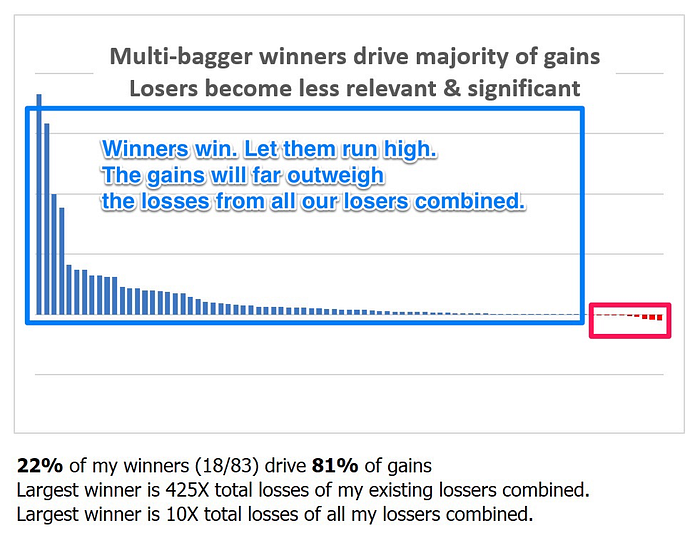

Investing performance need not be like a fair coin toss, in fact, we think our returns will tend to look like this, where the gains from our multi-bagger winners will more than offset all the losses from all our losers combined many folds over.

This is how our actual results end up looking, far more pronounced, and will likely could be even far more pronounced with time to come. The gains from our largest winner more than 10X all the losses from all our losers combined.

Winners become more relevant, and the losers become less so.

Investing is like a coin toss, just that it is a special one, and that’s also allowed us to keep beating the market thus far, and hopefully for many more years to come.

16 Jan 2020 | Eugene Ng | Founder & CIO| Vision Capital

Find out more about Vision Capital where we have beaten the market by more than 4X over the last 4 years: https://visioncapital.group/

Check out our recently published book on Investing, “Vision Investing: How We Beat Wall Street & You Can, Too!”. We truly believe that the individual investor can beat the market over the long-run. The book chronicles our entire investment approach. It explains why we invest the way we do, how do we invest, what we are we looking out for in the companies, where do we find them and when do we invest in them. It is available for purchase via Amazon, currently available via two formats, Paperback and eBook

Join my email list for more investing insights. https://visioninvesting.substack.com/

Follow me on Twitter @EugeneNg_VCap or Instagram @EugeneNg_VCap

This article is solely for informational purposes and is not an offer or solicitation for the purchase or sale of any security, nor is it to be construed as legal or tax advice. References to securities and strategies are for illustrative purposes only and do not constitute buy or sell recommendations. The information in this report should not be used as the basis for any investment decisions.

We make no representation or warranty as to the accuracy or completeness of the information contained in this report, including third-party data sources. The views expressed are as of the publication date and subject to change at any time.

Hypothetical performance has many significant limitations and no representation is being made that such performance is achievable in the future. Past performance is no guarantee of future performance.